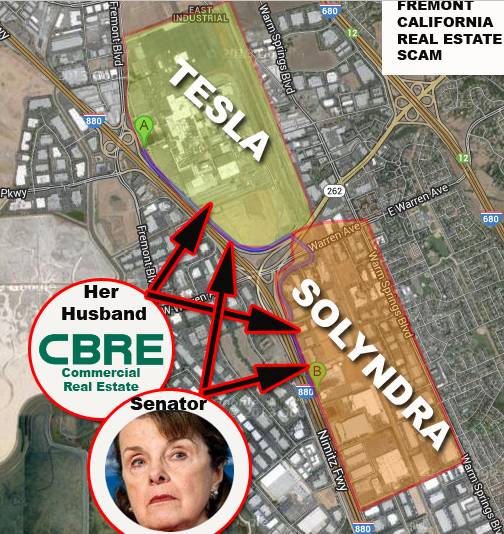

The 1% illuminati Lithium-Gate VC’s- Rigging Washington DC for profit at the expense of the public!

Who are the “Lithium ion VC’s”? Say “Howdy” to the ACTUAL 1% Illuminati!

Who are the “Lithium ion VC’s”? Say “Howdy” to the ACTUAL 1% Illuminati!

—————————————————————————-

“This matter has absolutely nothing to do with whether or not you like solar power or electric cars or gasoline or fracking or one technology over another. It has nothing to do with climate change; not a single thing. This is totally about banking, securities and finance fraud.

It is entirely about organized crime racketeering kickbacks arranged by arrogant frat-boy billionaires who sought to buy government, buy power, buy ego-trips, kill competitors and monopolize industries for personal gain in exchange for campaign efforts.”

– A U.S. Senate Source

—————————————————————————-

Watch the 60 Minutes episode: “The Cleantech Crash”, below, that began the series of 2014 expose events coming over the next 6 months:

[wpvideo jMnc6LJb]

The lobbyists called “Think Progress” (many of those targeted by investigations work, or worked there) and others, funded by the VC’s, have started massive spin to call it a bunch of lies and say that “No, No, it was really a big success”, but the facts, the criminal investigations and the money trail speak for themselves. It doesn’t matter if you are Democrat or Republican, it matters if you want billionaires buying your government and cutting you out of the loop.

D- LA Times

————————————————————————–

Now watch the 60 Minutes episode about how it was done:

http://www.youtube.com/watch?v=CHiicN0Kg10

[wpvideo fARepFlX]

———————————————————————–

The Democrats needed cash for the campaign. Democrats are always poor, so they never have enough money. The campaign staff went to the Silicon Valley Vc’s and said that if they paid for the campaign costs up front and rigged the search engines to only promote the Democrat candidates, then the campaign would give them $100 Billion of tax money that they would not have otherwise gotten, once the Democrats had control of the DOE slush fund. So they did, but they got caught by their greed, and now they need to go to federal prison.

It’s as simple as that!

E- Heritage

——————————————————————

Note From Victims: Multiple SOMO reporters/writers have spoken with a number of victims of this series of hits organized by the same group of people. If any major law firms (Multiple firms can file) begin the process of filing a class action RICO or damages action on behalf of the victims: Arrington, Assange, Eberhard, Brown, Conway, DM, Steve, Lakatos, Katie, AL, Etc… It is highly likely that a number of other victims (over 20+) will join the cases once they are filed and publicly noticed. Substantial evidence and testimony now exists and recoverable assets in potential court-ordered awards, from the attackers, exceed $50B+ in possible recoveries for damages caused by their organized efforts against these competitors and reporters. In other words, big class-action law firms, according to many plaintiff candidates: “if you file it, they will come.”

DFG, YY, DS, SAT/LAT/NYT

—————————————————————————–

Seriously…

…Don’t get your panties in a knot about saving electric cars or solar panels. They are NOT AT RISK. There are a ton of solar panel companies doing gangbuster business and you can buy all kinds of electric cars, from many companies, right now. Those things are safe. They are doing fine. Don’t let the VC media shills play your feel-good heart-strings. By complaining about political corruption you are not going to destroy the planet. You are going to destroy corruption. Got it? Green energy is doing fine but Corruption is also doing fine. Let’s stop the corruption and let the green energy keep on keepin’ on!

Bradley T- SF Chr

—————————————————————————–

Did they break the law? Multiple federal agency & committee probes now asked to look into organized crime charges over kickbacks.

The Westly Group (Under Investigation)

Ira “Linguini” Erenpries (Under Investigation)

Firelake Capital (Under Investigation)

John “Doe” Doerr (Under Investigation)

Kliener Perkins (Sued for Sexual Abuse)(Under Investigation)

Elon “The MuskRat” Musk (Sued on multiple charges of fraud by shareholders)

Steve “The Fix” Westly (Under Investigation)

Ray “The Sausage” Lane (Charged with Tax Fraud)

Steve Jurvetson (Under Investigation)

The Google Boys (Under Investigation)

Jonathan” Slippery” Silver (Fired) (Under Investigation)

Tom Perkins (Under Investigation)

Tim “I want-to-run-my-own-state” Draper (Under Investigation)

Draper Fisher (Under Investigation)

Vinohd Khosla and Connie Rice (Under Investigation, multiple documentaries)

Khosla Ventures (Under Investigation)

Tom “Fettucine” Styer (Under Investigation)

Steven “The Rat” Rattner (Indicted)

Raj “I-Am-Untouchable” Gupta (Indicted)

Hey Now… when you look at: their lobby hires, payment disclosures and blind SUPERPAC’s, which lithium ion interests they own or control and when you follow the money, it gets pretty ironic...

They are all friends of silicon valley’s “McKinsey” DOE Secretary of Energy Steven Chu; McKinsey DOE $$ Guy Matt Rogers & McKinsey DOE $$ Guy Steve Spinner (They paid to get them appointed). McKinsey staff have previously been put in Federal prison for rigging things, ie: Rajat Gupta.; and are under investigation world-wide.

They contracted a silicon valley consulting company called McKinsey Consulting and told McKinsey to write all these white papers for the White House and Federal Agencies that said: “lithium ion is the key to the future“. Then they bribed and influenced and “Revolving Door’d” to put Chu at DOE (Silicon Valley VC’s were the primary nominators of Chu per his nomination file docket) and they invested in all of the Lithium while their guy: Chu, (working with Rahm Emanual, Valarie Jarrett, David Axelrod and Robert Gibbs) handed out all of the taxpayer money to their investment projects. Easy Peasy. Scam.

Which Senator did they interact with the most? Which West Wing Chief of Staff?… See the latest Senate investigations and Class Action lawsuits for more. The Pope just hired McKinsey to fix “Vatican Corruption”.. Maybe not such a good idea?

Recordings and emails appearing soon. Many agencies, committees and media groups are now investigating, or have been asked to investigate by senior Congressional staff. Since Reid went “nuclear”, the gloves are off, it seems.

Do your own research. Check out every name mentioned and all of their past connections. Nowadays, it isn’t that hard to research. All of the parts of this have been mentioned in the mainstream press as of now.

Reporters asking to FOIA review the original Solyndra case # and case #’s hyphenated off of the Abound, Solyndra, and similar cases case #’s are having the best luck in story leads.

“One is building the new Bohemian Grove on the California coast at Half Moon Bay. One has started a Jr. Illuminati initiation program for young recruits that begins in the Stanford dorm rooms. One has publicly been charged with multiple crimes. One runs the technology suppression team for the NCVA. One has broken the record for hiring local escorts. Come watch the fun!

It’s non-stop hijinks with those crazy old boys from the Tech Branch of the Illuminati. Stay tuned for each episode of this made-for-tv romp that is guaranteed to be great fun for the whole family.”

Elon Musk, and these sorts of ego-maniac billionaires, do not care about regular people or customers. They exist for the joy they get in manipulating power and control and tend to do things like this:

[wpvideo jMnc6LJb]

[wpvideo 6syz0vNW]

[wpvideo h3AixjhD]

[wpvideo 6syz0vNW]

[wpvideo efQDTOLF]

[wpvideo fsB9480q]

[wpvideo QrKvoUyA]

KL, HJK, H, TH, JKL, PROPU- Denver News, LA Times, WSJ, BB, Susu

———————————————–

Silicon Valley: Satan’s Frat House?

Are Silicon Valley Angel Investors Colluding Over Deals? | Techdirt

Sep 22, 2010 … While there are plenty more angels in Silicon Valley than just 15, it is … Every industry has a dark side – most of us can’t see it and therefore, we forget its there. … VC investors would be wise to not attract the government with …

www.techdirt.com/ articles/ 20100921/ 18574611100/ are-silicon-valley-angel-investors-colluding-over-deals.shtml – View by Ixquick Proxy – Highlight

Tim Draper Wants To Split California Into Pieces And Turn …

Silicon Valley: Full of Arrogant-heads Who Hate San Francisco …

—————————————————

Steven Lawrence Rattner

(born July 5, 1952) is an American financier who served as lead adviser to the Presidential Task Force on the Auto Industry in 2009 for the Obama administration.[1]

New York Pension Fund Investigation

In 2005, Quadrangle made payments to private placement agent Hank Morris to help Quadrangle raise money for its second buyout fund.[13] Morris had come highly recommended to Rattner from U.S. Senator Charles Schumer.[14] Morris was also the chief political advisor to Alan Hevesi, the New York State Comptroller and manager of the New York State Common Retirement Fund (CRF), which invests in many private equity funds. Morris told Rattner he could increase the size of the CRF investment in Quadrangle’s second buyout fund. Rattner agreed to pay Morris a placement fee of 1.1% of any investments greater than $25 million from the CRF.[15]

In 2009, Quadrangle and a dozen other investment firms, including the Carlyle Group, were investigated by the U.S. Securities and Exchange Commission for their hiring of Morris. The SEC viewed the payments as “kickbacks” in order to receive investments from the CRF since Morris was also a consultant to Hevesi.[16] Quadrangle paid $7 million in April 2010 to settle the SEC investigation, and Rattner personally settled in November for $6.2 million without admitting or denying any wrongdoing.[17]

Prosecution by Attorney General Cuomo

The case drew significant media attention when Andrew Cuomo, the New York State Attorney General, demanded more severe penalties from Rattner than any of the other firms or individuals who had hired Morris as a placement agent.[18] Rattner was once a major fundraiser for Democratic Party candidates including Al Gore and Hillary Clinton, but Rattner had repeatedly passed on fundraising for Cuomo despite Cuomo’s past attempts to cultivate Rattner’s support.[19]

In an appearance on the Charlie Rose Show, Rattner asserted that hiring Morris as a placement agent was “legal then, legal now, and done properly.”[20] He explained he was willing to settle on reasonable terms as he had done with the SEC, but questioned whether Cuomo was motivated by the “facts” of the case and called Cuomo’s demands “close to extortion.”[21]

On December 30, 2010, Rattner reached a settlement with Cuomo to pay $10 million in restitution but no fines or penalties. He was not prohibited from continuing to protest his innocence.[22]

Wikipedia

———————————————————-

![]()

Ray Lane Rode Tech Boom Tax-Shelter Wave Broken by IRS

By Andrew Zajac & Jesse Drucker

The dot-com boom of the late 1990s has come back to haunt former Hewlett-Packard Co. (HPQ) Chairman Ray Lane.

Lane’s dispute with the Internal Revenue Service opens a window to a mostly bygone era when accounting and law firms conceived and sold tax-dodging strategies to investors seeking to avoid taxes on outsized gains from the still-swelling tech bubble.

A file photo shows Hewlett-Packard Co. former Chairman Ray Lane speaking during the Wall Street Journal ECO:nomics conference in Santa Barbara, California, during March 2011. Photographer: Jonathan Alcorn/Bloomberg

The shelters had memorable nicknames, based on acronyms: Son of BOSS, BLIPS, PICO and COBRA. Lane used one called POPS.

Then the IRS cracked down, triggering the kind of legal battles with the agency Lane is now embroiled in.

“Most of these types of tax shelters have flushed through the system,” said Bryan Skarlatos, a tax attorney at Kostelanetz & Fink LLP in New York. “The ones like you’re seeing with Lane are some of the stragglers.”

“It’s not the very last dinosaur caught in the tar pit, but it’s one of the last,” said Skarlatos, who represents clients in disputes with the IRS over POPS transactions.

Tax Bill

Lane, also the former president of Oracle Corp. (ORCL) and partner emeritus at venture-capital firm Kleiner Perkins Caufield & Byers, used POPS in an attempt to shield $250 million of income through what the IRS ruled were “sham” transactions.

Lane, 66, who left Oracle with more than $1 billion in stock and stock options in mid-2000, has agreed to settle with the IRS on a tax bill that could be as much as $100 million, even as he appeals the agency’s ruling in U.S. Tax Court in Washington. He said he fully paid his tax bill on sale of his Oracle options.

“My tax advisers put me into an investment,” he said in an interview. “Somewhere along the way I knew these things were being questioned by the IRS.”

The investment totaled $25 million, Lane said, and included an $18 million up-front payment used to fund startups.

A portion of that went to purchase warrants or stock options in five companies, including RocketGas Inc., Kleptomaniac.com. and Spectrum Target Detection Inc., according to a filing in one of at least five U.S. Tax Court cases involving Lane’s tax shelter investments.

Tech Startups

RocketGas was described in court papers as a business to “bring services traditionally available only at a gasoline station to customer’s home or office.”

Kleptomaniac.com was an “e-commerce solutions provider and e-tailing consultant” to brick-and-mortar retailers and Spectrum had developed a traffic radar gun that “was expected to replace traditional speed measuring devices used by law enforcement agencies.”

“Like most high tech startups which seemed so attractive in 2000, that high risk, high reward portfolio proved worthless within three years and petitioner simply seeks to recognize the real, hard-cash economic loss,” one of Lane’s lawyers argued in a court filing. Losses for the five companies totaled about $17 million, according to another filing.

The IRS argued that the investments in the companies “were payments of fees to promoters of listed and/or abusive tax avoidance transactions.”

Other Investors

Lane and other investors didn’t establish the value of stock options or warrants in an “amount greater than zero,” and as a result, no losses were allowable, IRS lawyers wrote.

Lane said the POPS shelter was assembled for him by Sidley Austin LLP, a Chicago-based law firm, the BDO Seidman consulting firm and Deutsche Bank AG, he said.

Deutsche Bank, Germany’s largest bank, admitted criminal wrongdoing in 2010 and agreed to pay $553.6 million to avoid prosecution over its participation in 15 fraudulent tax shelters, including POPS transactions.

The bank admitted to involvement in at least 1,300 deals, helping more than 2,100 customers evade about $5.9 billion in individual income tax on capital gains and ordinary income, according to a settlement agreement with the Justice Department.

Duncan King, a spokesman for Frankfurt-based Deutsche Bank, and Jerry Walsh, a spokesman for BDO, declined to comment on Lane’s remarks. Sidley Austin didn’t reply to phone and e-mail messages requesting comment.

Conspiracy Charge

BDO, now known as BDO USA LLP, said in June 2012 it would pay $50 million to settle a charge of tax-fraud conspiracy for helping wealthy individuals evade about $1.3 billion in taxes from 1997 to 2003.

In 2011, a jury convicted former BDO chief executive officer Denis Field and three others of more than 20 criminal counts including conspiracy and tax evasion.

A judge threw out Field’s conviction after finding that a juror lied about her past. A re-trial is pending.

POPS stands for Partnership Option Portfolio Securities.

Though it has multiple variations, a POPS transaction, in general, worked like this: an accounting firm would set up a series of partnerships, which would typically enter into transactions called straddles using foreign currencies.

Straddles involve simultaneously taking long and short positions to offset the investment risks.

Offsetting Loss

The partnership would sell off the position that generates the gain, which would be attributed to a partner that would be indifferent to the tax, such as a tax-exempt entity.

That would leave one of the partnerships with the offsetting loss.

An investor with a big gain somewhere else could then buy into the partnership and thus take advantage of the loss.

The IRS attacked such transactions for separating out the losses from the gains.

The IRS case against Lane’s Vanadium Partners LLC mentions “a series of meaningless steps,” involving a straddle, a tiered partnership structure and a transitory partner that allowed “a tax shelter investor to claim a permanent non-economic loss.”

Lane’s attorney, Charles Hodges, disputed the IRS contention that Vanadium was a sham that “lacked economic substance.”

In addition to the tech boom, conditions were ripe for tax shelters in the 1990s because the IRS had eased off enforcement under pressure from Congress, said Christopher Rizek, a lawyer at Caplin & Drysdale, a Washington-based law firm that specializes in tax matters.

Wealthy Individuals

“They spent about two years re-organizing themselves,” he said. “They were intimidated.”

By the mid-2000s more aggressive enforcement resumed.

Wealthy individuals who purchased POPS and other tax shelters were often identified by the IRS and Justice Department in probes of the accounting firms and law firms that sold them.

The uproar in Congress over whether the IRS tried to head off conservative groups from getting non-profit status could curb challenges to tax shelters again, Rizek said.

Tax lawyers are watching how the agency responds to “this month’s use as a pinata by Congress,” he said.

“They could be cowed again,” Rizek said. “We’ll see.”

The case is Vanadium Partners Fund LLC v. IRS, 9970-13, U.S. Tax Court (Washington).

To contact the reporter on this story: Andrew Zajac in Washington at azajac@bloomberg.net

To contact the editor responsible for this story: Michael Hytha at mhytha@bloomberg.net

——————————————————————

Vanity Fair tries to link Arrington rape accusation to Silicon Valley‘s …

Nov 1, 2013 … It claims that the scandal represents “the dark side of the Internet Age” … Maximillian Potter’s “Letter from Silicon Valley” in the December issue of Vanity Fair examines … And that was with a high profile VC firm to begin with.

www.zdnet.com/ vanity-fair-tries-to-link-arrington-rape-accusation-to-silicon-valley s-lack-of-women-in-tech-7000022702/ – View by Ixquick Proxy – Highlight

———————————————————————–

How the VC’s manipulated Afghanistan for Lithium HERE>>>

————————————————————————-

BLOOMBERG:

Tom Steyer: The Wrath of a Green Billionaire

By Joshua Green April 25, 2013

The billionaire — with a jar of tar sand oil

Billionaires get frustrated by Washington ineptitude just like everybody else. The difference is that they can afford to do something about it. Tom Steyer, who founded the San Francisco-based hedge fund Farallon Capital Management and retired last year with an estimated $1.4 billion fortune, is one such fed-up billionaire. Steyer’s particular grievance is the lack of government action to combat global warming. “If you look at the 2012 campaign, climate change was like incest—something you couldn’t talk about in polite company,” he says. “With the current Congress, the chance of any significant energy or climate legislation that would move the ball forward is somewhere around nil—possibly lower.”

So Steyer, 55, a major Democratic contributor, quit Farallon to devote his time and much of his money to changing this reality. In doing so, he’s joined an emerging class of billionaires—including this magazine’s owner, Michael Bloomberg and Facebook (FB) co-founder Mark Zuckerberg—who have forsaken the traditional approach of working through the political parties and instead jumped directly into the fray, putting their reputations and fortunes behind a cause.

Some environmental activists are thrilled. “In a country that’s dominated by billionaires gaming the political system for their narrow self-interest, it’s pretty neat to see a player who’s in it for the common good,” says author and environmentalist Bill McKibben. “He’s not a greedhead.” Many Democrats, McKibben among them, view Steyer as a liberal analogue of the conservative Koch brothers, the billionaire owners of Koch Industries, whose lavish support of free-market causes and political ruthlessness loom large in the liberal imagination.

Steyer’s financial commitment is unquestioned. In 2010 he and his wife, philanthropist Kat Taylor, signed the “Giving Pledge” begun by Warren Buffett and Bill and Melinda Gates to persuade wealthy people to devote the majority of their fortunes to good causes. That same year he spent $5 million successfully defending California’s greenhouse gas emissions law against a ballot measure, heavily financed by oil companies, to weaken it. He spent an additional $35 million last year on an initiative to close a tax loophole that benefited out-of-state corporations. Voters approved the measure, which will raise $1 billion a year in new revenue for the state, in November. “He has made a difference in California,” says Representative Henry Waxman, the Los Angeles Democrat.

His aptitude for hardball politics is less certain. On March 18, Steyer, a vocal opponent of the proposed Keystone XL pipeline that would pump tar sands oil from Canada to the Gulf Coast, clumsily inserted himself into the Massachusetts Democratic primary race between Representatives Edward Markey and Stephen Lynch for the state’s open Senate seat. Channeling John Wayne, Steyer penned a bullying letter demanding that Lynch renounce his support for the pipeline “by high noon” a few days later or face the wrath of all the opposition Steyer and his checkbook could muster. Lynch’s campaign dismissed the stunt as “billionaires

issuing ultimatums.” The Boston Globe chastised Steyer for butting into a race in which both candidates had pledged to eschew PAC support. Markey probably doesn’t even need the support:

But after the searing defeat in Congress three years ago of legislation to cap carbon emissions, Steyer and many other Democrats preoccupied with climate change are convinced that only a smash-mouth, confrontational style of politics can save the planet. He subscribes to the analysis offered in a recent paper by Harvard sociologist Theda Skocpol that the loss derived from Democrats’ naive faith that their best chance at climate legislation was cooperating with polluters on a grand bargain negotiated by Washington power brokers. The strategy failed to account for Republicans’ radicalization and use of the filibuster. And because environmental groups had neglected to organize, no grassroots pressure materialized when the legislation stalled.

Steyer confidently presents himself as being in the vanguard of a hardheaded new approach. “The way politics works is by people winning and losing jobs—their own jobs,” he says. “Until people running for office believe it’s in their own interest, that it will make them popular with their constituents to stand up for good policy, it’s not going to be good politics.” For now, this approach entails rounding up a posse of environmental activists and making blustery threats to keep Democrats in line. Earlier this month, Steyer paid for an airplane to circle a Boston Red Sox game at Fenway Park trailing a banner that read, “Steve Lynch for Oil Evil Empire.”

—————————————————————————————–

Team Obama Releases List of Campaign Bundlers…Corrupt Jon Corzine and Solyndra Goons Steve

Spinner/Steve Westly Top the List

February 1, 2012 by Scotty Starnes

What a list of corruption. Ex-Democrat Senator Jon Corzine is on the list. Corzine bankrupted MF Global and stole hundreds of billions from investors. Steve Spinner is an Obama bundler who pushed the Solyndra loan and Steve Westly has received billions for corporations he has ties to. Remember, Obama pretended to hate lobbyist as he issued waivers for lobbyists to work in his administration.

WASHINGTON (AP) — President Barack Obama’s re-election campaign identified its top fundraisers on Tuesday, including 61 people who each raised at least half a million dollars. Altogether, the more than 440 fundraisers collected at least $75 million to help Obama win a second term.

Among them are embattled former New Jersey Gov. Jon Corzine. Obama’s campaign and the Democratic National Committee late last year returned $70,000 in contributions from Corzine and his wife following questions about the collapse of MF Global, the financial firm Corzine ran.

…The list includes two fundraisers linked to Solyndra LLC, theCalifornia solar company that received a $528 million federal loan and then later declared bankruptcy, prompting a federal investigation. Steve Spinner, an Energy Department adviser, raised at least $500,000 and Steve Westly, a venture capitalist who was an unpaid adviser to the department, raised between $200,000 and $500,000.

…Though Obama rejects contributions from lobbyists, his top fundraisers include

individuals involved in the business of influencing government.

Michael Kempner, among those who raised more than $500,000, is president and CEO of MWW Group, a public relations firm with a large lobbying business. Kempner himself is not a registered lobbyist.

Sally Susman, another fundraiser in the $500,000-plus category, is executive vice president for policy, external affairs and communications at Pfizer Inc., a job that includes directing the pharmaceutical giant’s government relations operations.

Spinner and Westly are lobbyist as well. They bundled money for Obama then lobbied for money to be invested in corporations they have interest in.

———————————————————

Obama releases list of top money ‘bundlers’

Associated Press

By JIM KUHNHENN and KEN THOMAS February 1, 2012 9:32 AM

WASHINGTON (AP) — President Barack Obama’s re-election campaign identified its top fundraisers on Tuesday, including 61 people who each raised at least half a million dollars. Altogether, the more than 440 fundraisers collected at least $75 million to help Obama win a second term.

Among them are embattled former New Jersey Gov. Jon Corzine. Obama’s campaign and the Democratic National Committee late last year returned $70,000 in contributions from Corzine and his wife following questions about the collapse of MF Global, the financial firm Corzine ran.

Corzine is no longer raising money for the re-election, campaign officials said.The campaign divided the list into four groups based on how much money donors raised:

$50,000-$100,000, $100,000-$200,000, $200,000 to $500,000 and those who raised more than $500,000 apiece.

The donors represent a broad network of contributors, many of them longtime Democratic Party stalwarts.

The list includes two fundraisers linked to Solyndra LLC, the California solar company that received a $528 million federal loan and then later declared bankruptcy, prompting a federal investigation. Steve Spinner, an Energy Department adviser, raised at least $500,000 and Steve Westly, a venture capitalist who was an unpaid adviser to the department, raised between $200,000 and $500,000.

The disclosure came as Obama headed back out on the money trail, speaking Tuesday night at two high-dollar fundraisers in the Washington area where donors paid $35,800 per ticket to see him. At an event at the posh St. Regis Hotel, the president told donors that Republicans have “the wrong vision for America,” though he didn’t mention any of his opponents by name or reference the voting under way in Florida, where polls were closing in the state’s GOP primary.

Obama said voters needed to know “that this is not an abstract ideological argument, that this is a practical concrete argument,” and that the election is about whether they’ll be able to find a good job with a living wage and get health care for their families. “They’ve got to feel that we are actively advocating on their behalf.”

Obama’s campaign ended the year with more than $81 million in the bank, but Republicans are gearing up in the race for the White House.

The Republican National Committee collected $27 million during the final three months of 2011, compared with $23 million by the DNC. In December, the RNC raised $11.6 million while the DNC collected $8.8 million.

Through the end of 2011, the RNC had $20 million in the bank and $13 million in debt, while the DNC held $12.5 million in cash on hand and $6.5 million in debt.

Though Obama rejects contributions from lobbyists, his top fundraisers include individuals involved in the business of influencing government.

Michael Kempner, among those who raised more than $500,000, is president and CEO of MWW Group, a public relations firm with a large lobbying business. Kempner himself is not a registered lobbyist.

Sally Susman, another fundraiser in the $500,000-plus category, is executive vice president for policy, external affairs and communications at Pfizer Inc., a job that includes directing the pharmaceutical giant’s government relations operations.

California figured most prominently on Obama’s roster of big money “bundlers.” Sixteen are from California and 13 are from New York.

Top fundraisers include movie producers Jeffrey Katzenberg and Harvey Weinstein, and Vogue editor-in-chief Anna Wintour. Actress Eva Longoria was in the second highest tier, bundling $200,000 to $500,000 for Obama’s re-election.

Associated Press writer Erica Werner contributed to this report.

————————————————————–

D- LAT, GH- WAPO, HJ-HuffPO, Surf Alliance- FGT,

——————————————————————-

Trolling the illuminati!

According to all of these studies, and general consensus, people who drive Tesla’s are arrogant pricks.

According to all of the studies, and general consensus, about Silicon Valley Billionaires, they, too are arrogant pricks.

Arrogant Fraternity House prick boys are the most entitled, egotistical pseudo-macho people on Earth.

Ergo, they will defend their sports team, beer brand, stock portfolio and anything that questions their penis-size, to the death.

So, if you are trying to drain the illuminati’s bank accounts in order to achieve a political advantage, there is no greater gift than Tesla Motors.

By Elon Musk’s own published admission, Tesla was dead in 2008. It was only kept alive as The Walking Dead by Silicon Valley VC’s in order to get battery kickback deals and policy control.

Every time the Tesla stock ticker starts dropping like a rock, when real investors realize it is a scam, the Silicon Valley VC’s run out and buy a bunch of stock to make it look like Tesla has risen from the stock market dead in spite of the fires, recalls, management walk-outs, employee accidents, fraud charges, lawsuits and all of the other things that would kill any other company in the stock market. (Is that legal?)

That is called “pumping the stock“. Those are fake stock buys from Silicon Valley VC’s.

The only thing is, the more they pump, the poorer they get.

T. C. – BB

———————————————-

http://www.youtube.com/watch?v=PFvKQhQzZPI

————————————————-

Ha! In San Francisco they are rioting against Google’s buses, everybody hates the entitled freaks (“Hipsters”) from Silicon Valley and Silicon Valley has become the most un-cool thing on the planet because of all the personal data harvesting and that spy thing. As usual, Obama is 2 weeks behind in his news updates, he mentioned “Silicon Valley” in his press conference today as if that was a good thing. It is lucky he is firing most of his staff, that never told him what was really going on. Somebody better tell tell him that The Valley is a very negative brand item these days. No wonder Silicon Valley wants to succeed from California: Everybody hates them!

Dione- H

————————————————–

You know those secret organizations that form conspiracy cartels to

You know those secret organizations that form conspiracy cartels to

control government and industry. Here are all of the members of one such

organization known, among the members, as “The Omni” (Or Illuminati-East- Coast). Research them, draw a line between the connections. See what you see:

- Rockmark Corporation

- Fedmark Corporation

- EC Holdings, Inc.

- ECW Investor Associates

- Realrock I

- Louis R. Benzak

- John R.H. Blum

- James R. Bronkema Trust

- Vincent deP. Farrell, Jr.

- Leslie H. Larsen

- Bill F. Osborne

- Portman Family Trust

- William F. Pounds

- David Rockefeller

- DR & Descendants, L.L.C.

- The Estate of Edna B. Salomon

- Robert B. Salomon

- Ralph B. Salomon

- William G. Spears

- George M. Topliff

GH-LAT

—————————————————————————————–

Protesters Stop Apple And Google Buses – Business Insider

8 hours ago … Protesters in San Francisco have stopped a bus filled with Apple employees on their way to work. They’ve also stopped a Google bus in …

www.businessinsider.com/protesters-an-apple-bus-2013-12 – View by Ixquick Proxy – Highlight

Bus Vandalized as Protesters in S.F., Oakland Target Silicon Valley …

5 hours ago … Update 2 p.m.: Our local “Google bus” protests took a turn today as a total of … In San Francisco, a bus carrying Apple employees was blocked …

blogs.kqed.org/ newsfix/ 2013/ 12/ 20/ eviction-protesters-oakland-san–francisco-target-silicon-valley-buses – View by Ixquick Proxy – Highlight

Apple/Google Busses stopped by protesters in San Francisco – SlashGear

7 hours ago … After stopping a Google bus two weeks ago, a group of protesters from what appears to be the same organization has stopped a bus full of …

www.slashgear.com/ applegoogle-busses-stopped-by-protesters-in-san–francisco-20309571/ – View by Ixquick Proxy – Highlight

Protesters swarm tech worker shuttle buses in Oakland, S.F. | Other …

4 hours ago … Chris Roberts/The S.F. Examiner; Protesters block an Apple shuttle bus … Apple, Google, Yahoo, Genentech or eBay – “they’re all the same to …

www.sfexaminer.com/ sanfrancisco/ protesters-swarm-tech-worker-shuttle-buses-in-oakland-sf/ Content?oid=2655001 – View by Ixquick Proxy – Highlight

—————————————————

How Silicon Valley‘s Tech Reign Will End – Slashdot

Jun 29, 2013 … And Silicon Valley isn’t like a city, it’s like a… … and a lot of talk about VC funding for “great ideas”, which are all just Yet Another Social …… It sucks. It’s not actually a city, it’s more like a long series of 80s era malls which have …

www.slashdot.org/ story/ 13/ 06/ 29/ 1643246/ how-silicon-valleys-tech-reign-will-end – View by Ixquick Proxy – Highlight

Scaling Venture Capital? We suck. We can do better. | 500 Startups

Apr 6, 2012 … Because we SUCK at EXACTLY the thing we’re supposed to help … past 20+ years i’ve spent in Silicon Valley as an engineer, entrepreneur, …

www.500.co/2012/04/06/scaling-venture-capital/ – View by Ixquick Proxy – Highlight

5 Reasons to Move Your Startup Out of Silicon Valley — Tech News …

Sep 10, 2008 … The weather sucks in some of these towns (not Tallahassee) so your … In the Valley, every VC has a portfolio company in each flavor – their …

www.gigaom.com/ 2008/ 09/ 10/ 5-reasons-to-move-your-startup-out-of-silicon-valley/ – View by Ixquick Proxy – Highlight

Fred Wilson on why corporate VCs suck | PandoDaily

Jun 18, 2013 … And two of my favorite moments were about the venture capital business. … You’ re Lucky, Twice You’re Good: The Rebirth of Silicon Valley and …

www.pando.com/2013/06/18/fred-wilson-on-why-corporate-vcs–suck/ – View by Ixquick Proxy – Highlight

The Underbelly of Silicon Valley: VC “Finders” – peHUB

VC conference organizers should make their profits from sponsors, not from struggling … Last week, a Silicon Valley investor named Hugh Sloan III came across a …. securities – it would suck to pay for advice that leads one to break the law.

www.pehub.com/2010/02/the-underbelly-of-silicon-valley–vc-finders/ – View by Ixquick Proxy – Highlight

Silicon Valley Could Use A Downturn Right About Now | TechCrunch

May 22, 2007 … Silicon Valley is paradise for geeks, and people flock here from all over the world … but for the most part there wasn’t a lot of venture capital moving into new web … Times are good, money is flowing, and Silicon Valley sucks.

www.techcrunch.com/ 2007/ 05/ 22/ silicon-valley-could-use-a-downturn-right-about-now/ – View by Ixquick Proxy – Highlight

Most Venture Capital Firms Suck – Slate

May 7, 2012 … It’s well known that if you invest in actively managed stock funds, then the fund manager is going to make out a lot better than you will. Less well …

www.slate.com/ blogs/ moneybox/ 2012/ 05/ 07/ most_venture_capital_firms_suck.html – View by Ixquick Proxy – Highlight

Dave McClure is ripping VCs again: They’re f***ing arrogant and …

Aug 22, 2012… B.C. today, the founder of Silicon Valley‘s 500 Startups dropped the F-bomb … He added that the returns for venture capital “absolutely suck.

www.geekwire.com/ 2012/ dave-mcclure-rips–vcs-fing-arrogant-stupid-aholes/ – View by Ixquick Proxy – Highlight

Why does everything suck?: Arrington, Race, and Silicon Valley

Oct 28, 2011 … I spent this summer in Silicon Valley as part of the NewMe Accelerator. … To be clear, I am not saying any VC says at a partner meeting, “you …

www.whydoeseverythingsuck.com/ 2011/ 10/ arrington-race-and-silicon-valley-i.html – View by Ixquick Proxy – Highlight

How We Ruined Silicon Valley | Motherboard

Long an oasis of innovation and meritocracy, Silicon Valley has often represented all that is pure in capitalism, a place where guys dare to … If you were a good VC you could make $100 million. … It’s not like anybody is doing evil or bad.

motherboard.vice.com/ blog/ facebook-marks-the-end-of-silicon-valley-as-we-know-it – View by Ixquick Proxy – Highlight

Sift Science Funded to ‘Fight Evil on the Internet’ – Venture Capital …

Mar 19, 2013 … Venture Capital Dispatch HOME PAGE » …. Featuring the VentureWire reporting team in the Silicon Valley, New York, Boston and Shanghai …

blogs.wsj.com/ venturecapital/ 2013/ 03/ 19/ sift-science-funded-to-fight-evil-on-the-internet/ – View by Ixquick Proxy – Highlight

Rude VC: Copying Silicon Valley – Rude Baguette

Mar 5, 2013 … For a more in-depth review, A History of Silicon Valley by Piero Scaru. … the emergence of Silicon Valley, in large part by trying to do no evil.

www.rudebaguette.com/2013/03/05/rude-vc-copying-silicon-valley/ – View by Ixquick Proxy – Highlight

Michael Arrington, Jenn Allen, and the Dark Side of the Information …

Dec 1, 2013 … Speakers are a Who’s Who of Silicon Valley and in recent years … first female engineer, and Ben Horowitz, co-founder of the V.C. leviathan …

www.vanityfair.com/ business/ 2013/ 12/ michael-arrington-jenn-allen-relationship – View by Ixquick Proxy – Highlight

Silicon Valley should wake up to clawback culture — Tech News …

Jun 28, 2011 … Silicon Valley should wake up to clawback culture … the culture of Silicon Valley venture capital and the clubby world of private equity: ….. conclusion that they are , by their very nature, evil or intended to cheat shareholders.

www.gigaom.com/ 2011/ 06/ 28/ silicon-valley–should-wake-up-to-clawback-culture/ – View by Ixquick Proxy – Highlight

John Doerr – Wikipedia, the free encyclopedia

His success in venture capital has garnered national attention; he has been and is … Doerr is a high profile supporter of the Democratic Party in Silicon Valley.

en.wikipedia.org/wiki/John_Doerr – View by Ixquick Proxy – Highlight

Welcome to the (Don’t Be) Evil Empire | Common Dreams

Jun 25, 2013 … The criticism of Silicon Valley is long overdue and some of the … Google, the company with the motto “Don’t be evil,” is rapidly becoming an empire. …. is extremely unequally distributed, and current venture capital is going …

https://www.commondreams.org/view/2013/06/25-3 – View by Ixquick Proxy – Highlight

The Dark Side of Silicon Valley – Center for Computer Research in …

And some of the industry’s most prominent venture capitalists, the financiers of the high- … This is a series about the dark side of the Silicon Valley miracle.

https://ccrma.stanford.edu/~dattorro/Silicon%20Valley.pdf – View by Ixquick Proxy – Highlight

Down and out in Silicon Valley: The dark side of easy VC access …

Sep 21, 2011 … Down and out in Silicon Valley: The dark side of easy VC access … The Valley is the tech centre of the Universe and you’re unlucky if you’re not …

www.ventureburn.com/ 2011/ 09/ down-and-out-in-silicon-valley-the-dark–side-of-easy-vc-access/ – View by Ixquick Proxy – Highlight

WATCH: If Nikola Tesla Pitched Silicon Valley VCs | Inc.com

May 31, 2013 … WATCH: If Nikola Tesla Pitched Silicon Valley VCs BY Mark Suster …. two-time entrepreneur who has gone to “the dark side” of venture capital.

www.inc.com/ mark-suster/ if-nicola-tesla-pitched-silicon-valley–vc.html – View by Ixquick Proxy – Highlight

Silicon Valley is no meritocracy – Vivek Wadhwa – The Kernel

Dec 19, 2011 … I learned that virtually all of Silicon Valley‘s venture capital firms are …. These are blunt comments, and exemplify the dark side of Silicon Valley.

www.kernelmag.com/ features/ essay/ 160/ silicon-valley-is-no-meritocracy/ – View by Ixquick Proxy – Highlight

The dark side of VC positivity | The Venture Company

Dec 8, 2010 … Only 45 of 790 U.S. VCs make any consistent money for LPs (according to a reputable Silicon Valley money manager). So, Venture as a …

www.venturecompany.com/blog/2010/12/the-dark–side-of-vc-positivity/ – View by Ixquick Proxy – Highlight

The Grassy Road: The dark side of Silicon Valley

Jun 18, 2012 … Silicon Valley is on a roll right now. The relatively low levels of capital needed to start a software company has meant that start up incubators …

pennyherscher.blogspot.com/2012/06/dark–side-of-silicon-valley.html – View by Ixquick Proxy – Highlight

Are Silicon Valley Angel Investors Colluding Over Deals? | Techdirt

Sep 22, 2010 … While there are plenty more angels in Silicon Valley than just 15, it is … Every industry has a dark side – most of us can’t see it and therefore, we forget its there. … VC investors would be wise to not attract the government with …

www.techdirt.com/ articles/ 20100921/ 18574611100/ are-silicon-valley-angel-investors-colluding-over-deals.shtml – View by Ixquick Proxy – Highlight

Modern Luxury | San Francisco Magazine | Dark side of the boom

Feb 17, 2012 … E.B. Boyd reports on how his death has touched a nerve in Silicon Valley—and forced one of its biggest secrets out in the open. E.B. Boyd …

www.modernluxury.com/san-francisco/story/dark–side-of-the-boom – View by Ixquick Proxy – Highlight

How Scientists and Engineers Got It Right, and VC‘s Got It Wrong …

Jul 25, 2011 … ESL, the first company I worked for in Silicon Valley, was founded by a … however, the dark side to the current startup environment in the bay …

www.steveblank.com/ 2011/ 07/ 25/ how-scientists-and-engineers-got-it-right-and-vc%E2%80%99s-got-it-wro ng/ – View by Ixquick Proxy – Highlight

A Tale From The Dark Side Of Silicon Valley PowerAgent was …

Apr 13, 1998 … The list of investors included venture capital firms Information … Today Sundby, 45, lives on Silicon Valley‘s dark side–a place where there are …

money.cnn.com/magazines/fortune/fortune_archive/1998/04/13/240866/ – View by Ixquick Proxy – Highlight

Silicon Valley: What’s the dark side of Silicon Valley? – Quora

I’m talking about the stuff you don’t read on TechCrunch. … It is amazingly difficult to start/have a family if you make “normal” salaries here (you …

www.quora.com/Silicon-Valley/Whats-the-dark–side-of-Silicon-Valley – View by Ixquick Proxy – Highlight

DOUBLE-CROSSED / Silicon Valley entrepreneurs say they have …

Nov 17, 1999 … The power of Silicon Valley‘s top venture capitalists is rivaled only by the … But the High-tech miracle has a dark side: untold stories of ruined …

www.sfgate.com/ bayarea/ article/ DOUBLE-CROSSED-Silicon-Valley-entrepreneurs–say-2896276.php – View by Ixquick Proxy – Highlight

The Arrogant VC: Why VCs are disliked by entrepreneurs – Venture …

Dec 27, 2009 … And yes, I also plan on writing a feature about the “good side” soon… … on the VC side who have behaved in a rude and disrespectful manner“. … Continued in Part 2 with unwanted advice, arrogance, and the dark side of the force… …. you realize that Entrepreneurs in Si

www.venturehacks.com/articles/arrogant-vc – View by Ixquick Proxy – Highlight

Oil barons and tech hipsters share a dark side. – Slate

Jan 7, 2013 … Cozy relationships are common in Silicon Valley too. Marc Andreessen, whose venture capital firm routinely sells smaller companies to tech …

www.slate.com/ blogs/ breakingviews/ 2013/ 01/ 07/ oil_barons_and_tech_hipsters_share_a_dark_side.html – View by Ixquick Proxy – Highlight

You’d Better Shop Around: Doing Due Diligence on Your VC …

Aug 2, 2011… about the dark side of the venture world; stories of VCs who weren’t … VC partner doesn’t have an obvious bit of Silicon Valley pedigree?

www.xconomy.com/ san-francisco/ 2011/ 08/ 02/ youd-better-shop-around-doing-due-diligence-on-your-vc/ – View by Ixquick Proxy – Highlight

Vulture Capital: Mark Coggins: 9781460979471: Amazon.com: Books

A trip through the dark satanic mills of venture capital with Chandler or Hammett as … believable story about the dark side of Silicon Valley‘s start-up community.

www.amazon.com/Vulture-Capital-Mark-Coggins/dp/1460979478 – View by Ixquick Proxy – Highlight

With friends like these … Tom Hodgkinson on the politics of the …

Jan 13, 2008 … Facebook is a well-funded project, and the people behind the funding, a group of Silicon Valley venture capitalists, have a clearly thought out …

www.theguardian.com/technology/2008/jan/14/facebook – View by Ixquick Proxy – Highlight

————————————————————————–

The Billionaire illuminati Front Groups

If the group has the words: “Grassroots”, “Citizens”, “Taxpayers”, “Occupy” or other such warm/cozy buzzwords in it’s title assume, that it may be a pretend front group for a billionaire, a corporation or a union. in the last 20 years, according to state and federal campaign disclosures: 98.2% of all such campaign groups were paid for by just a handful of men on behalf of their special interests. Look deeper, check the SUNSHINE sites and know what is what. Don’t get suckered by, either left or right wing facades. They apply to ALL parties. Do your research before you sign up, give money, phone tree or march for one or the other.

Koch Industries: Secretly Funding the Climate Denial Machine …

Billionaire oilman David Koch used to joke that Koch Industries was “the biggest … Koch Front Groups Attack RGGI—The Regional Greenhouse Gas Initiative …

www.greenpeace.org/ usa/ en/ campaigns/ global-warming-and-energy/ polluterwatch/ koch-industries/ – View by Ixquick Proxy – Highlight

Enron billionaire expands craven plot to abuse workers – Salon.com

Oct 7, 2013 … A billionaire‘s scheme to loot public workers’ pensions now includes a shadowy front group — and brand-new target.

www.salon.com/ 2013/ 10/ 07/ enron_billionaire_expands_craven_plot_to_abuse_workers/ – View by Ixquick Proxy – Highlight

Political activities of the Koch brothers – Wikipedia, the free …

They actively fund and support organizations that contribute significantly to ….. a huge network of foundations, think tanks, and political front groups. Indeed … ” Covert Operations: The billionaire brothers who are waging a war against Obama .”.

https://en.wikipedia.org/ wiki/ Political_activities_of_the_Koch_brothers – View by Ixquick Proxy – Highlight

Americans for Prosperity – SourceWatch

Americans for Prosperity created an offshoot front group called Patients United Now, …. According to a 2010 article on Koch Industries and the billionaire Koch …

www.sourcewatch.org/index.php?title=Americans_for_Prosperity – View by Ixquick Proxy – Highlight

Brendan DeMelle: Study Confirms Tea Party Was Created by Big …

Feb 11, 2013 … A new academic study confirms that front groups with longstanding ties to the tobacco industry and the billionaire Koch brothers planned the …

www.huffingtonpost.com/ brendan-demelle/ study-confirms-tea-party-_b_2663125.html – View by Ixquick Proxy – Highlight

The Billionaires Behind Newt’s ‘American Solutions For Winning The …

Jul 29, 2008 … The same old men that propelled George W. Bush into office in 2000 and 2004 are behind Newt Gingrich’s multimillion-dollar front group, …

www.thinkprogress.org/ climate/ 2008/ 07/ 29/ 174099/ newt-aswf-billionaires/ – View by Ixquick Proxy – Highlight

The Libertarian Billionaire Agenda Propelling the Tea Party Monster …

Oct 3, 2013 … The small handful of oil and Wall Street groups behind the Tea Party, groups like FreedomWorks and Americans for Prosperity, were all front …

www.alternet.org/ tea-party-and-right/ libertarian-billionaire-agenda-propelling-tea-party-monster-has-shut- down – View by Ixquick Proxy – Highlight

empathyeducates – Exposed: The Billionaire-Backed Group Strong …

Another backer is billionaire John Arnold, a former Enron trader who ….. Why would Mary do the bidding of a corporate front group, pouring her energy and time …

www.empathyeducates.org/ exposed-the-billionaire-backed-group-strong-arming-parents-into-destr oying-their-kids-public-schools/ – View by Ixquick Proxy – Highlight

American Task Force on Palestine finds funding from anti …

Nov 27, 2013 … The fairly recent establishment of the pro-Israel front group, Scholars for Peace in the Middle East (SPME) was also made possibly by …

www.mondoweiss.net/2013/11/palestinian-billionaire-repressive.html – View by Ixquick Proxy – Highlight

George Soros – Discover the Networks

Multi-billionaire funder of leftwing causes and groups; Founder of the Open …… “ to justify repressive measures” on the home front while “establish[ing] a secure …

www.discoverthenetworks.org/individualProfile.asp?indid=977 – View by Ixquick Proxy – Highlight

“Fix the Debt” Shows Its True, Billionaire-Funded, Anti-Tax Colors

Dec 3, 2012 … Fix the Debt has a very clear position on tax rates for millionaires, billionaires, and corporations, right there in the group’s “Core Principles” …

www.ourfuture.org/ 20121203/ fix-the-debt-finally-shows-its-true-billionaire-funded-anti-tax-color s – View by Ixquick Proxy – Highlight

Articles from VCR:

———————————————————————

THE EXPOSE ON “THE SUMMIT ON THE FUTURE OF EXPONENTIAL TECHNOLOGIES”.

The Silicon Valley Tech-illuminati hold an event called the “SUMMIT ON THE FUTURE OF EXPONENTIAL TECHNOLOGIES” organized by The Singularity University (Which is dedicated to merging people with machines and creating SkyNet, or something like it)(Notice that Google just bought a humanoid robotics company as they infest the entire internet so the actual Terminators must be only a few years away.)

At SUMMIT ON THE FUTURE OF EXPONENTIAL TECHNOLOGIES they discuss “3D printing living hookers on demand”. Imagine, you are horny and you can print up Marilyn Monroe or Angelina Jolie for pleasure and, later, “reprocess” your pseudo-flesh pleasure-lifeform into another character. Silicon Valley VC’s love disposable people. Ask any H1B engineer from India. They like to get them in, get the code and shoot them back to Bhopal so the VC’s don’t have to pay them any stock. Already one of the leading employers of escorts and prostitutes in the U.S., disposable 3D printed sex people couldn’t be more perfect for Silicon Valley.

They discuss the economics of “In-Vitro Hamburgers“. They claim to have already made, and eaten In-Vitro Hamburgers. Short on cash?, give birth to In-Vitro hamburger patties and sell them to McDonalds to supplement your income. Great! So now the Silicon Valley VC’s really can eat their young.

While they were at it, they also arranged to have Coca Cola control our last natural

resource: Drinking water. The Singularity people made a deal so only Coca Cola can get you fresh water if you are dying from thirst. Evil?

People are actually building these things. The Illuminati pay for this crap. How out of touch with reality can these billionaires be?

Here the rich and powerful fraternize with their anointed “inventors”. These “inventors” are ivy league college chums that they fund in order to control markets. Pitched as, the “next generation of technological break-through”, these backers tend to support things that Austin Powers wants more than the average person needs. Closely aligned with the audaciously self-promoting yuppie TED Talk culture, these gatherings are college parties for mutual admiration indulgences.

At least with TED Talks you can go online and watch TED Talks to research who the

arrogant self-obsessed Silicon Valley hipsters are. With the SUMMIT ON THE FUTURE OF EXPONENTIAL TECHNOLOGIES, it is a bit more stealthy but NPR snuck in and got the goods.

Famous scientist Craig Vettner says Singularity hype is all: “Bu*lSh*t” in an NPR

interview. He, and most credible engineers find that this is all pump and dump stock

shilling.

AT- University of Los Angeles

———————————————————-

AI or BS??

http://ask.metafilter.com/162790/AI-or-BS

—————————————————————

See this link for more:

https://www.growvc.com/openTalks/publicBoard/22779

————————————————————————

See this link for other thoughts:

http://37signals.com/svn/posts/1927-the-next-generation-bends-over

————————————————————————–

Here is why they tried to “KILL” Micheal Arrington, Martin Eberhard, Snowden, Assange and the rest:

So A Blogger Walks Into A Bar…

Michael Arrington

Tuesday, September 21st, 2010

Yesterday I was tipped off about a “secret meeting” between a group of “Super Angels” being held at Bin 38, a restaurant and bar in San Francisco. “Do not come, you will not be welcome,” I was told.

So I did what any self respecting blogger would do – I drove over to Bin 38, parked my car and walked in.

in the back of the restaurant in a private room was a long oval table. Sitting around the table, Godfather style, were ten or so of the highest profile angel investors in Silicon Valley. These investors, known as “super angels” because they have mostly moved on to launch small venture funds of their own, are all friends of mine. I knew each person in the room very, very well.

I certainly didn’t think anything was amiss and I expected a friendly hello and an invitation to sit down for a drink or two before being shooed off while they talked about whatever they thought should be kept off record. But instead it went something like this:

Me: Hey!

Person who was talking: oh, oh no.

Me: Hi. I heard you guys were here and I wanted to stop by and say hi.

Them: dead silence.

Me: so….

Them: Deafening silence.

Me: This is usually where you guys say “sit down, have a drink.”

Them: not one sound

Me: This is awkward. I guess I’ll be leaving now.

I’ve never seen a more guilty looking group of people. But that alone isn’t that big of a deal. Lively conversations often die quickly when I arrive, and I’ve learned not to take it personally. But I did sniff around a little afterwards, and have spoken to three people who were at that meeting. And that’s where things got interesting.

This group of investors, which together account for nearly 100% of early stage startup deals in Silicon Valley, have been meeting regularly to compare notes. Early on it was mostly to complain about a variety of things. But the conversation has evolved to the point where these super angels are actually colluding (and I don’t use that word lightly) to solve a number of problems, say multiple sources who are part of the group and were at the dinner. According to these souces, the ongoing agenda includes:

- Complaints about Y Combinator’s growing power, and how to counteract competitiveness in Y Combinator deals.

- Complaints about rising deal valuations and they can act as a group to reduce those valuations.

- How the group can act together to keep traditional venture capitalists out of deals entirely

- How the group can act together to keep out new angel investors invading the market and driving up valuations.

- More mundane things, like agreeing as a group not to accept convertible notes in deals (an entrepreneur-friendly type of deal).

- One source has also said that there is a wiki of some sort that the group has that explicitly talks about how the group should act as one to keep deal valuations down.

At least two people attending were extremely uneasy about the meetings, and have said that they are only there to gather information, not participate.

So what’s wrong with this?

Collusion and price fixing, that’s what. It is absolutely unlawful for competitors to act together to keep other competitors out of the market, or to discuss ways to keep prices under control. And that appears to be exactly what this group is doing.

This isn’t minor league stuff. We’re talking about federal crimes and civil prosecutions if in fact that’s what they’re doing. I had a quick call with an attorney this morning, and he confirmed that these types of meetings are exactly what these laws were designed to prevent.

I’m not going to say who was at the meeting since at least a couple of the attendees are saying they were extremely uncomfortable with the direction the conversation was going. But like I said, it included just about every major angel investor in Silicon Valley.

On a side note, this is a difficult post to write, because I call nearly every person in that room a friend. But these actions are so completely inappropriate it has to be called out.

———————————————————————————-

Not sure what your sources are, but courts have ruled that parallel action can be sufficient evidence of conspiracy under Section 2 of the Sherman Act. See e.g. American Tobacco v. United States (1946), available here:

http://supreme.vlex.com/vid/american-tobacco-v-united-states…

The Supreme Court wrote:

“[The conspiracy’s] existence was established, not through the presentation of a formal written agreement, but through the evidence of widespread and effective conduct on the part of petitioners in relation to their existing or potential competitors.”

If I remember correctly from my anti-trust class last year, the American Tobacco precedent still stands. You don’t need written or audio evidence to get a conviction; anti-competitive behavior in the marketplace is sufficient.

—–

dandelany 774 days ago | link

Interesting questions… IANAL, but I imagine they’re colluding to bring down the valuations of startups, therefore essentially fixing the “price” of their money, to be paid for in startup equity.

If I, and others, say your company is worth a million dollars, then I’m fixing the price of my $500,000 at 50% of your company.

—–

brendonjason 774 days ago | link

IANAL(E), but this scenario would seem to be more of a concern if startups in Silicon valley got together over dinner to deny deals that didn’t offer similar terms and prices in dollars for securities of all startups represented at said dinner simultaneously.

As for angels fixing the “price of their money” I don’t understand how antitrust applies to this anymore than it would to, say, how LIBOR is determined.

If antitrust applies to colluding on the dollar amount to be paid OUT instead of price asked for money coming in, then if I start a boycott of something (colluding to pay $0) am I guilty of violating antitrust laws?

As I understand it (not much, I admit), antitrust applies to goods and services, not cost of money. If antitrust applied to cost of money, the Federal Reserve would not exist since it’s basically an extension of the member banks that make up its institutional board of directors (not board of governers). All they do is get together and fix the price of money to be printed and lent out to member banks.

Also, this whole “I stumbled in on a secret meeting of powerful men conspiring to start a revolution” thing is somewhat suspect; throughout history this gambit, if it actually happened that way, is usually either desperate grab at 15 minutes of fame (which seems unlikely given Michael’s popularity), an attempt to gain instant credibility on some esoteric but useful new subject (“I was the only outsider privvy to what happened there, so you can trust me”) or, unfortunately, a cynical move feigned by the men in the room to inspire hasty and possibly faulty reactionary stances by the supposed target of their “envy”.

I could be wrong though. I just can’t believe guys who are careful enough to get to such a position in life would all simultaneously get so careless. On the same day. In the same place.

—–

polynomial 773 days ago | link

> if I start a boycott of something (colluding to pay $0)

http://j.mp/dividedby0

(Unless of course you actually get them to give it to you for nothing, which is generally not the point of a boycott…)

—–

jeromec 774 days ago | link

Think of the stock market. That’s certainly a marketplace. It’s made up of investors seeking to earn a return on their money by investing in companies. Think of the illegalities involved in collusion to manipulate the stock market. Now think of Silicon Valley as a less formal/regulated stock market…

With Groupon nobody is asked to not buy or otherwise participate in the market unless done through Groupon.

Instead, it’s like a grocery store co-op; members pool their money to get more buying power. This doesn’t mean they agree to refrain from shopping elsewhere, as that would be collusion/conspiring to produce a market effect.

IANAL

—–

brendonjason 774 days ago | link

If I have an investing club and we come to define an investment approach, say, what stocks we like and what we think they should be valued at, are we colluding to price fix the market? If I think a company is over priced and I am in charge of executing trades for my investing club, whose members unanimously agreed not to buy the stock in question until it fell down say, $20 more in price – are we colluding? Yes. Colluding to price fix? No. We’re simply colluding not to participate in the buy side. That may or may not lead to sellers slowly changing their asking price. But that’s a two-way street. I don’t see the illegality according to anti-trust. Now if every major instututional house/hedge/mutual/pension fund that owned that stock got together and colluded to refuse to SELL us any stock until we agreed to their higher price, that I understand is illegal. They are fixing the price literally. But I don’t see how us refusing to participate in a transaction on the buy side is illegal whether we have 5 members or 5 million.

Saying that the angels are colluding to price fix buys into Michael’s assertion that “together, the men in that room account for nearly 100% of all angel deals”. That means that their “deals” are the commodity in question, and they are free to do as they wish. If it’s their money, then it’s hard to make the claim that their money is the market. There’s certainly more money in the world than theirs.

—–

blueben 774 days ago | link

“Look, you and I both know your company is worth $50 million. But I only want to pay $10 million, and I’ve already worked out a deal with my competitors so they won’t bid any more than that either. We own the market for investment, so you can take it or your company can die for lack of funding.”

You don’t see a problem with this kind of artificial market manipulation? This is no longer a market; it short circuits true capitalism and only serves to siphon gains from the seller (in this case, the company’s founders) to the buyer, who will turn around and effectively try to resell (or otherwise exit) the company for profit.

Everyone seems to be convinced that price fixing only applies to sellers. That’s wrong. It firmly applies to both selling and buying. It’s fundamentally about market manipulation; taking steps to undermine the economy of the system for direct personal gain. That kind of behavior destroys wealth and erodes confidence in the marketplace.

—–

aufreak3 774 days ago | link

I’m ignorant enough to have the same question in my mind.

—–

SkyMarshal 774 days ago | link

Grellas, what’s your take on this Quora comment? In a nutshell, it’s not illegal for collusion on the buy side, only the sell side:

Tarun Nimmagadda, Mutual Mobile Co-Founder, COO

http://www.quora.com/Who-are-the-Super-Angels-that-Michael-A…

“The article was a fun read, but it is a false claim that this is illegal. Collusion, price fixing, and dividing markets is only illegal on the selling side. Think about how people and groups are able to band together for purchasing power and special treatment when buying goods/services. Its not illegal.

Worth noting thought that if this price manipulation happened in relation to a company with over a 100 investors, SEC regulations would begin to apply and this behavior would be illegal”

—–

grellas 774 days ago | link

That comment was made out of ignorance. Antitrust laws are by no means limited to sellers only.

—–

SkyMarshal 774 days ago | link

Interesting, thanks.

—–

Alex3917 774 days ago | link

“Collusion, price fixing, and dividing markets is only illegal on the selling side.”

IANAL, but didn’t Standard Oil got broken up largely for being a monopsony? In fact the first two complaints from the DoJ were about sell-side issues:

“Rebates, preferences, and other discriminatory practices in favor of the combination by railroad companies; restraint and monopolization by control of pipe lines, and unfair practices against competing pipe lines; contracts with competitors in restraint of trade; unfair methods of competition, such as local price cutting at the points where necessary to suppress competition; [and] espionage of the business of competitors, the operation of bogus independent companies, and payment of rebates on oil, with the like intent.”

—–

invisible 774 days ago | link

I know this was pointed at grellas, but I think this is a misunderstanding when we look at price fixing and collusion. The illegality of collusion is secretly forming agreements to benefit competitors at the expense of other parties. Words like defraud can succinctly help you understand whether it is illegal or not when looking at these agreements.

—–

dctoedt 774 days ago | link

The Wikipedia summary of Section 1 of the Sherman Act is a decent read:

http://en.wikipedia.org/wiki/Sherman_Antitrust_Act#Violation…

—–

—–

jon_dahl 774 days ago | link

Grellas, would there have to be evidence that the participants were acting anti-competitively, or is being in the room enough? Arrington says that a few of the folks there were uncomfortable with what was going on, and were maybe there just to see what was happening.

—–

grellas 774 days ago | link

Assuming the meeting had an illegal purpose (which is a major assumption at this point), one might infer that anyone present was complicit in that illegal purpose. In my view, that by itself would not normally be enough to subject someone to liability, especially if the participant disclaims affiliation with the group and thereafter does not act in concert with it.

—–

guelo 774 days ago | link

Does it matter if the participants have monopoly power over the market? I have a hard time believing Arrington’s claim that “ten or so” angels control “nearly 100% of early stage startup deals in Silicon Valley”. If they control lets say only 50% of this market would it still be illegal collusion?

—–

grellas 774 days ago | link

It is not required that the participants have monopoly power for them to transgress the law on this point. I agree with you that the “nearly 100% of the early stage deals in Silicon Valley” statement is wildly overstated but this should not affect the fundamental legal analysis here.

—–tc 774 days ago | link

Congratulations to PG & company. When I first met Paul years ago, he was musing about spam filters and the finer points of a well-designed lisp. Now he apparently has the top 10 angels in Silicon Valley running scared of him.

—–

jeromec 774 days ago | link

The interesting thing is unlike that group of Angels apparently in the bar PG’s interests are less about helping himself, and more about helping entrepreneurs. From an essay by PG entitled “Why YC”: The real reason we started Y Combinator is one probably only a hacker would understand. We did it because it seems such a great hack. There are thousands of smart people who could start companies and don’t, and with a relatively small amount of force applied at just the right place, we can spring on the world a stream of new startups that might otherwise not have existed.

In a way this is virtuous, because I think startups are a good thing. But really what motivates us is the completely amoral desire that would motivate any hacker who looked at some complex device and realized that with a tiny tweak he could make it run more efficiently. In this case, the device is the world’s economy, which fortunately happens to be open source.

http://paulgraham.com/whyyc.html

—–

wensing 774 days ago | link

YC’s greatest hack is identifying founder material based on technical rather than social proof (the YC app asks for an example of the coolest thing you’ve ever built, not an example of a cool person that thinks you are cool). This hack is possible thanks to a judges panel full of real nerds. How many super angels or VC’s can claim to have the same?

—–

gruseom 774 days ago | link

I agree that YC are able to identify great hackers and great founders more easily because they are these things themselves. What’s little recognized is how big a difference this is between YC and the other YC-like funds.

—–

wensing 774 days ago | link

Yes. I had a colleague apply for TechStars and her takeaway from the interview was “he was really focused on where the business was.” Doesn’t seem in line with what I’ve heard about YC’s primary interest (it’s not the business model).

—–

gruseom 774 days ago | link

It seems kind of obvious that most successful startups don’t succeed via the business model they started with. And that great founders can change business models more easily than great business models can change founders. Thesethings are so obvious that they’re cliches, in fact, but that doesn’t mean that they’re common practice.

—–

qq66 774 days ago | link

I don’t think anybody’s stated interests should be taken as an indicator of their true interests. In this case,with PG, I do believe that his stated intentions are sincere. But there is often so little correlation between actual and stated intentions, that I don’t take any such statement at face value.

—–

jeromec 774 days ago | link

I don’t think anybody’s stated interests should be taken as an indicator of their true interests. I agree. (actually I’d replace “taken as an indicator” with “taken as an absolute indicator”) In this case, with PG, I do believe that his stated intentions are sincere. I agree.

—–

mhendrick 774 days ago | link

Correct me if I’m wrong, but isn’t it likely that the angels involved also make up a strong percentage of the people who invest on Demo Day in post-YC companies? How can it be a “PG vs Angels” situation when the parties involved are likely some of YC’s portfolio companies biggest “supporters”?

—–

brc 774 days ago | link

One of the outputs from the YC process is better educated founders who have a lot more guidance in negotiating through a deal Even if the deal flow was exactly the same, just having the founders suffering less from information assymetry would be a stone in the shoe of the Angels. Think of it this way : if YC did all the same things, but also turned founders into being Angel patsies at dealtime, do you think they would be upset about it? I would guess it’s the information about how to negotiate, and what a good deal looks like is the problem. I’m sure they love the concept of demo-day to go deal shopping, but would prefer it if the products didn’t talk back.

—–

MediaSquirrel 774 days ago | link

YC is the seller, angels at Demo Day are the buyers. Just cuz you work with someone closely doesn’t mean you won’t or can’t try to screw them.

—–

redrobot5050 774 days ago | link

Yeah. I mean, look at the JooJoo/CrunchPad Debacle. According the Mike A., that’s exactly what happened.

—–

mhendrick 774 days ago | link

Agreed. It’s possible they got a bit overconfident in their respective positions because of the easy access to so many well-vetted companies.

—–

jeromec 774 days ago | link

Correct me if I’m wrong, but isn’t it likely that the angels involved also make up a strong percentage of the people who invest on Demo Day in post-YC companies?

Yes, I believe so.

How can it be a “PG vs Angels” situation when the parties involved are likely some of YC’s portfolio companies biggest “supporters”? That question might be better put to those Angels in the bar…

—–

mhendrick 774 days ago | link

I’m not defending the angels involved by any means; I actually think it’s a great thing that this has been exposed if it is indeed what’s been going on. The easy access to YC companies may in fact be what emboldened them to act in this manner in the first place. Once this all plays out, I think it’s safe to assume that at least a few of the angels in question are going to have to answer for their actions. Should be interesting to hear what they have to say.

—–

brendonjason 774 days ago | link

Yes. They are running scared of the growing threat of the Ylluminati. But since they have 100% of all the deals, they also seem to co-invest(?!?).

These anxious (yet all-powerful) group of angels and this unstoppable new seed-stage prominence. They form a closed loop. A loop closed off to venture capitalists and angels not at that meeting … which is basically everybody.

Except Michael. He got away with his life intact and lived to warn us all. Actually, I don’t know what’s scarier – the supposed collusion or the subtle dread that Y Combinator is supposed to evoke in my mind as I ponder the possibility of this event being true. If it is true – maybe we should be side with these poor angels and help them before it’s too late. To paraphrase Woodrow Wilson, “Since I entered (angel investing), I have chiefly had (angel investor’s) views confided to me privately. Some of the biggest men in the (Valley), in the Field of (IT) and (Venture Capital), are afraid of something. They know that there is a power somewhere so organized, so subtle, so watchful, so interlocked, so complete, so pervasive, that they better not speak above their breath when they speak in condemnation of it.” That something … is Y Combinator.

Um … no. The dark side doesn’t suit you, Y Combinator.

Please stop.

I’m sorry. Maybe I’ve had too many beers tonight. But this is the kind of scenario that only comes out of the mind of a silicon valley PR firm.

(please don’t downvote me too much … I’d like to get above 100 karma points just once for a change! Noooo!)

—–

limist 774 days ago | link

I upvoted you just for the historical reference.

—–

mixmax 774 days ago | link

So a blogger gets a tip from a source, knows the people involved, acts on it and smells a rat. He sticks around and talks to a few people he knows, makes a few calls and gets a breaking story. Sounds to me like bloggers are the new journalists and that traditional media is in big big trouble.

—–

sachinag 774 days ago | link

Felix Salmon does this, and he’s a blogger working for Reuters. Dan Primack does this, and he’s a blogger working for Fortune. It’s not about old/new media – it’s about hustle.

—–

Alex3917 774 days ago | link

Read Manufacturing Consent or any of the books that have been written about the MSM since then. It’s very much about old media verse new media.

If this were the NYT they’d probably tell Arrington he couldn’t run the story because it’d interfere with either their ad sales or else their access to sources. For example, just look at how/why they covered up their knowledge of the warrantless wiretapping until after Bush got reelected.

Whereas with Arrington there’s no one to tell him he can’t do it because it’s his blog, and because he’s not part of some mega corporation the chances of a story like this killing the revenue of some part of his empire are infinitely lower.

—–

metamemetics 774 days ago | link